Your right to choose your repairer

“It’s your car, and you have a right to choose where it is repaired. Your insurer is obliged to pay for all reasonable costs of the repair.” That is the legal position according to the Office of Fair Trading.

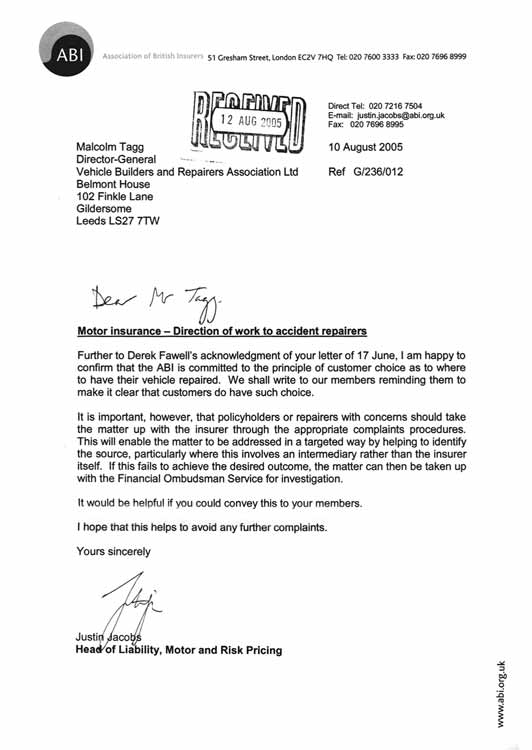

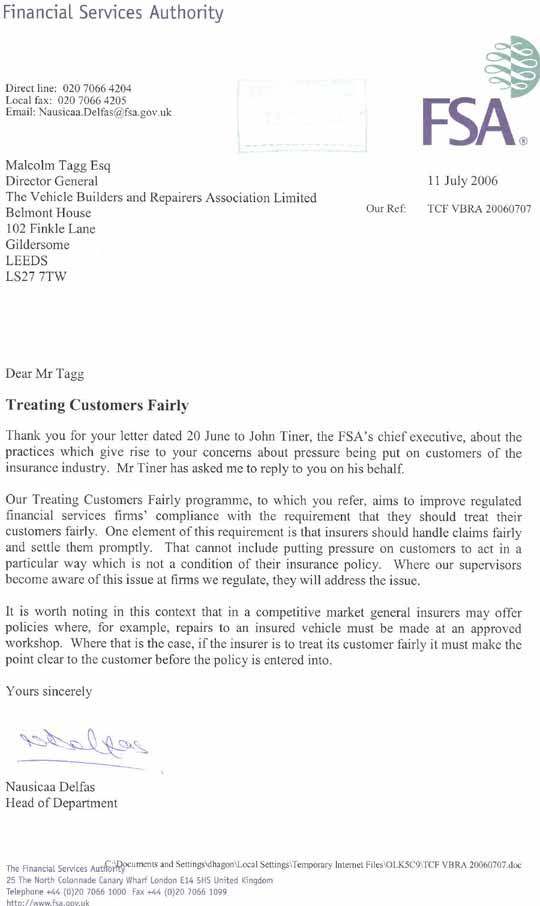

Your insurer may try and divert you to a repairer that provides them with special discounts or kickbacks – they may refer to such a repairer as “Approved” or “Authorised”, (suggesting that any other repairer is somehow “Unapproved” or “Unauthorised”). While your insurer may recommend a repairer to you, in most situations it is illegal for them to try to pressure you to use their choice of repairer. The Association of British Insurers , the Director-General of the VBRA, the Office of Fair Trading, and the Financial Services Authority have all confirmed their agreement on this point.

If your insurer does try to pressure you into using their choice of repairer, the FSA consider this a significant ethics breach, and you can report this matter to them.

Insurers have been known to tell their customers that they will suffer delays, get no guarantee, or not have access to a courtesy car if they choose their own repairer. These statements are all false – it is illegal for the insurer to introduce a delay if their preferred repairer is not used, the guarantee is provided as normal by the customer’s choice of repairer (we provide the full ChipsAway warranty), and a courtesy car, where needed, can also be provided by the repairer.

To arrive at your premium, your insurer calculates your risk (based on factors such as your age, gender, occupation, claim history, home postcode and vehicle performance group).

If you have earned a no-claims discount, this gives a percentage to be deducted to give a final premium.

Making a claim usually reduces earned discount by two years’ worth (and you do not earn discount for the year in which you claim).

Drivers with four or five years of no-claims can pay extra to ‘protect’ their no-claims discount, which is then not reduced if they claim. However if they claim this is still reflected in their claim history which is one of the factors that the insurer uses when calculating the base premium. In other words, claiming on your insurance puts your premiums up, even if you have a protected no-claims discount – something insurers can be less than up-front about.

Your claim history can also be reflected by premium increases in other insurance policies for which you are a driver – for example a second car or motorcycle, a spouse’s car on which you are a named driver, or a company car policy – the premiums for all these policies will be loaded as a result of your new claim history, despite the claim not being in relation to that vehicle. Failing to mention the claim to the insurers on the other policies can invalidate the other policies completely!

Insurers can load your premium based on a claim by around 20% of the claim value, for as long as five years. This means that once a driver has paid the excess amount on their policy, and then budgeted for five years of increased premiums, it is often the case that it would be cheaper for them to pay for repairs privately, and not claim on their insurance at all. A bodyshop repair can cost thousands in the long run, even when repairs are supposedly covered by insurance!

ChipsAway repairs are different. They often cost less than even the excess amount on a typical insurance policy, making a claim unnecessary, restoring and preserving the value of the vehicle while ensuring the professional finish expected from the world’s leading network in bodywork repair.

ChipsAway’s modern techniques mean a lower claim value even when an insurance claim is the only way for a driver to fund repairs. Simply put, whether you are claiming on your insurance or not, whether you have protected no-claims or not – choosing ChipsAway Cambridge can save you money!

You are not required by law (unless you were explicitly told otherwise when taking out your policy) to use your insurer’s repairer, or to collect multiple quotes that they then choose from. If you want ChipsAway Cambridge to carry out your insured repairs, we can forward our quote to your insurer. They are then legally obliged to pay for your ChipsAway repairs unless they can show that the cost of doing so is unreasonable.

If you require any assistance in deciding whether you should claim on your insurance, or with managing your claim, contact us – we can help.

You're just a few short steps away from fixing that damage!

Get My Free Estimate

{kind=link}

{kind=link}